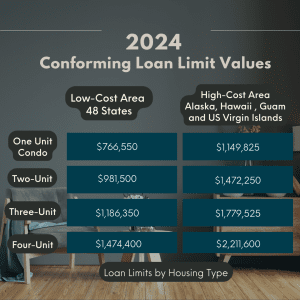

Conventional Loans

What is a Conventional Loan?

By definition, a conventional loan is any mortgage that is not guaranteed or insured by the federal government. A conventional loan is generally referring to a mortgage loan that follows the guidelines of government sponsored enterprises (GSE’s) like Fannie Mae or Freddie Mac. Conventional loans may be either “conforming” and “non-conforming.” Conforming loans follow the terms and conditions set by Fannie Mae and Freddie Mac. Non-conforming loans don’t meet Fannie Mae or Freddie Mac guidelines, but they are also considered conventional.

Whether you’re buying a home or want or refinance your mortgage, a Conventional Loan might be right for you. If you’re unsure about your credit rating, or have concerns about a down payment, Conventional Mortgages can give you piece of mind with low-closing costs and flexible payment options.

What are the Conventional Loan Requirements?

To decide if you qualify for a Conventional Mortgage Loan, we will look at:

- Your income and your monthly expenses. Standard debt-to-income ratios are 28/36 for Conventional Loans. These ratios may be exceeded with compensating factors.

- Your credit history (this is important, but Conventional’s credit standards are flexible). A FICO score of 620 or above is very helpful in obtaining an approval.

- Your overall pattern rather than individual problems you may have had.

To be eligible for a Conventional mortgage, your monthly housing costs (mortgage principal and interest, property taxes and insurance) must meet a specified percentage of your gross monthly income (28% ratio). Your credit background will be fairly considered. At least a 620 FICO credit score is generally required to obtain a Conventional approval. You must also have enough income to pay your housing costs plus all additional monthly debt (36% ratio). These percentages may be exceeded with compensating factors.

What are the Conventional Down Payment Requirements?

Conventional Loans require the home buyer to invest at least 5% – 20% of the sales price in cash for the down payment and closing costs. If the sales price is $100,000 for example, the home buyer must invest at least $5,000 – $20,000.

What will my Interest Rate be?

The interest rate for your home loan will be determined by the type of loan program that you qualify for and your credit score

What types of property are eligible?

While Conventional Mortgage Guidelines allow you to purchase warrantable condos, planned unit developments, modular homes, manufactured homes, and 1-4 family residences. Conventional Loans can be used to finance primary residences, second homes and investment property.

Can I get a Conventional Mortgage Loan after bankruptcy?

Criteria for Conventional loan approvals state that if you have been discharged from a Chapter 7 bankruptcy for four years or more, you are eligible to apply for a Conventional mortgage. If you have had a Chapter 13 bankruptcy, it must be documented that your credit reputation has been re-established for at least two years to be eligible for a Conventional Loan Application.

What kinds of loans do Conventional Programs Offer?

Fixed rate loans – Most Conventional Mortgages are fixed-rate mortgages. In a fixed rate mortgage, your interest rate stays the same for the entire loan period. With a fixed rate Conventional Mortgage, you always know exactly how much your monthly payment will be. Contact us for today’s Conventional mortgage rates.

Adjustable rate loans – With a conventional adjustable rate mortgage (ARM), the initial interest rate and monthly payments are low, but these may change during the life of the loan.

© 2016 – 2023 Absolute Mortgage & Lending NMLS# 1910591

© 2016 – 2023 Absolute Mortgage & Lending NMLS# 1910591